This article was first published on the WeChat public account: Hong Kong stocks. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

Editor's note: The pharmaceutical industry has always been a key part of the market. Regardless of the market, there is no shortage of investors' attention. In recent years, with the deepening of medical reform, the industry's reforms have begun, and the value of innovative drugs is particularly evident at this stage. Important, the innovation-driven pharmaceutical companies enjoy the valuation premium, A-share pharmaceutical leader Hengrui Medicine 600276, stock bar and H-share pharmaceutical leader Shijiazhuang Group have all gone out of independent strong market, the value is always compared, in the current time node In the context of the increasingly close interconnection between China and Hong Kong, it is particularly important to look at the value of the two. Today, I share the Gloen columnist: Wang Ke's comparison of the two ideas for investors' reference.

In recent years, with the aging of society, the pressure on medical insurance expenditure has been increasing. At the same time, the Chinese economy has entered a new normal, the growth rate of medical insurance income has slowed down, and people’s awareness of the quality of medical services and medicines has increased. The reality of the low level of commercial insurance development in China determines that it is impossible to become the main body of medical insurance expenditure in the short and medium term, so the direction of medical insurance reform is particularly eye-catching.

Many contradictions are entangled together, and fees must be guaranteed to ensure that quality becomes an inevitable choice for new medical reforms. Industry policies are frequent, and it is not to achieve the above objectives, such as bidding price reduction, consistency evaluation, strict control of drug proportion, two-vote system, Restricted medications, new medical insurance catalog adjustments, etc. The adjustment of the policy is reflected in the capital market, that is, the performance of different types of pharmaceutical listed companies varies widely. Those who rely on the large number of approvals and have a strong marketing ability, the traditional Chinese medicine injections and generic products are single and the subsequent products are insufficient. Poor, innovative pharmaceutical companies have been favored by investors.

At present, the gap between domestic pharmaceutical companies and international giants is obvious, but with the internationalization of high-end technical talents, the progress of basic research, the improvement of technology, the frequent exchange of academics at home and abroad, and the continuous investment in research and development funds, many domestic drugs Enterprises such as Hengrui Medicine and Shijiazhuang Group have begun to lead the Chinese medicine 600056. China's wisdom." Innovative pharmaceutical companies have attracted the attention of more and more investors. Typical representatives include Hengrui Medicine in the A-share market, Shijiazhuang Group in the Hong Kong stock market, and China Bio-Pharma.

Let's take a simple comparison between the Shijiazhuang Group in the Hong Kong stock market and Hengrui Medicine in the domestic A-share market. Review the restructuring process of the two companies, their strategic layout, existing product lines, R&D reserves, growth paths, and hidden concerns. Analyze and compare many aspects in order to have a deeper understanding of the two.

I. Comparison of changes in the company's operating system

1.1 Shijiazhuang Group

On August 21, 1997, Shijiazhuang Group Co., Ltd. was jointly established by Hebei Pharmaceutical Group, Shijiazhuang Yipiao Group, Shijiazhuang Second Pharmaceutical Group and Shijiazhuang Four Medicine Co., Ltd. Cai Dongchen is the chairman and general manager.

On June 16, 2007, Legend Holdings and Shijiazhuang City State-owned Assets Supervision and Administration Commission formally signed a property rights transfer agreement to acquire 100% of the state-owned property rights of Shijiazhuang Group at a price of 870 million yuan.

In 2008, Legend Holdings transferred its entire shareholding in Shijiazhuang Group to the Phase III fund of its subsidiary, Hony Capital.

On June 27, 2012, China National Pharmaceutical Group (later renamed Shijiazhuang Group) announced that it will acquire Hongyi, the major shareholder at a total consideration of HK$8.98 billion, including Shijiazhuang Group, Ouyi, and Shijiazhuang Group. Assets including Wei.

In 2013, Hony Capital began to sell shares in Shijiazhuang and sold it in 2015. After the transaction was completed, the company's chairman and CEO Cai Dongchen became the actual controller, and the shareholding ratio reached about 30%. The group completely realized privatization and the transformation of stone medicine was completed.

Five years after the completion of the restructuring of Shijiazhuang Group, the company has achieved good results in its business performance and capital market. Since 2013, the company's revenue growth rate has increased from 9.949 billion Hong Kong dollars to 12.369 billion Hong Kong dollars in 2016, an increase of 24.32%, but its net profit has increased from 973 million Hong Kong dollars to 2.101 billion Hong Kong dollars, an increase of 115.93. %. The company's product structure has been greatly optimized and has now transformed into one of the most innovative pharmaceutical companies in China.

In terms of market capitalization, before the issuance to major shareholders in June 2012, the market value was less than 3 billion. After the completion of the issuance, the market value was about 12 billion. The current market value is about 73 billion, which is about 500% in five years.

Shijiazhuang Group's 2010-2017 stock price performance

|

1.2 Hengrui Medicine

In 1970, the predecessor of Hengrui Medicine, Lianyungang 601008, was established as a pharmaceutical factory.

In 1990, Sun Feiyang became the director of the factory, and it was on the verge of bankruptcy. After hard work, he became a well-known enterprise in the field of anti-tumor in China, and the benefits improved.

In 1997, Hengrui Pharmaceutical carried out a share reform and introduced China Pharmaceutical Industry Corporation, Lianyungang Pharmaceutical Industry Corporation Trade Union, Lianyungang Pharmaceutical Purchasing and Supply Station, and Kangyuan Pharmaceutical Co., Ltd. as shareholders.

Listed on the Shanghai Stock Exchange in 2000, it is still state-owned after listing, and Sun Feiyang has no shareholding.

On March 22, 2003, the state-owned shareholder Hengrui Group signed an equity transfer agreement with Tianyu Medicine, Zhongtai Trust and Lianyungang Hengchuang Technology. Tianyu Pharmaceutical became Hengrui Pharmaceutical as the largest shareholder with a shareholding ratio of 27.15%. Subsequently, Sun Feiyang became the actual controller of Tianyu's conditions and became the actual controller of Hengrui Medicine.

In June 2006, Hengrui Pharmaceutical's share-trading reform was completed, and Tianyu Pharmaceutical (later renamed Jiangsu Hengrui Pharmaceutical Group) entered Hengrui Medicine with a holding ratio of 24.6%.

In the ten years after the completion of the share reform, Hengrui Pharmaceutical has achieved excellent results both in terms of business performance and performance in the capital market. In 2006, Hengrui Pharmaceutical's annual revenue was 1.42 billion yuan, net profit was 200 million yuan, and its market value was about 3 billion yuan. In 2016, Hengrui Pharmaceuticals' revenue was 11.09 billion yuan, and its net profit was 2.589 billion yuan, an increase of 6.8 times. And 11.9 times; the company's total market value increased from about 3 billion in 2006 to 160 billion in September 2017, an increase of more than 50 times.

Hengrui Medicine 2006-2017 stock price trend

|

1.3 Summary

From today's perspective, for the restructuring of Shijiazhuang Group and Hengrui Medicine, the sale price of state-owned shares is indeed low. For example, Tianyu Pharmaceutical (later renamed Hengrui Pharmaceutical Group) acquired a 27.15% stake in Hengrui Medicine and spent a total of about 226 million. Yuan, the market value of this part of the stock is about 800 million yuan, but in the context of the "national retreat and the people", it is still compliant. From the final result, after the completion of the enterprise restructuring, both the performance and the market value of the enterprise have achieved rapid growth, and local governments, management, employees, and investors are beneficiaries. Even from the perspective of local governments that have suffered from the damage at the beginning of the restructuring, the taxation and employment created by the enterprises that have grown and developed can already be compensated.

This does not deny the positive effect of state-owned holdings on the development of enterprises. In fact, in quite a number of industries, it can still achieve good operating results under the conditions of state-owned holdings. For pharmaceutical companies, especially chemical and biopharmaceutical companies, innovation is the guarantee for sustainable development, and innovation success depends to a large extent on the correct and continuous investment of the company's high-level strategic decision-making, the technical strength and execution of the team. Every link faces a high level of risk. The primary goal of state-owned capital is to preserve value, and then to increase value. The high-risk and high-yield business model matches the private capital with the strongest risk-taking ability. In the operation of innovative pharmaceutical companies, the most suitable role of state-owned capital is to retain The status of minority shareholders or complete withdrawal.

2. Comparison of existing product lines and core varieties

2.1 Shijiazhuang Group

The products of Shijiazhuang Group mainly include six series of nearly 1,000 varieties including cardiovascular and cerebrovascular, anti-tumor, antibiotic, vitamin, antipyretic and analgesic, and digestive system medication. The “Enbpuâ€, which has been successfully listed, is the first-line drug in the field of stroke treatment, and is the third class of new drugs with independent intellectual property rights in China. New drugs such as NBP, Xuan Ning, Ou Lining, Jin Youli and Duomei also have excellent performance after being listed.

Among the core products of Shijiazhuang Group, Enbpu's revenue exceeds 2 billion, Ou Laiing's income exceeds 1 billion, and Xuan Ning's income is about 500 million. Multi-American is expected to become a heavy variety of more than 500 million in 2017. Force and Norining also have great potential in the future.

NBP enters the 2017 medical insurance catalogue, and in the future sales in overseas markets, the variety is expected to become the first heavyweight drug in China's innovative pharmaceuticals with annual sales of US$500 million to US$1 billion.

|

Data source: company's 2016 annual report, sample hospital data speculation, company's official website

2.2 Hengrui Medicine

The main products of Hengrui Medicine cover anti-tumor drugs, surgical anesthesia drugs, special infusions, contrast agents, cardiovascular drugs and many other fields. Hengrui Medicine has an absolute advantage in the field of anti-tumor, and is one of the few companies in China that can compete with foreign giants. The company is also strong in surgical anesthesia and contrast agents, with several heavyweights over 1 billion. In addition to generic drugs, the innovative drugs Ericoxib and apatinib have been approved, of which apatinib achieved about 300 million in revenue in 2015 and more than 1 billion in 2016.

Hengrui Pharmaceutical has more than 500 million and 1 billion heavyweights, which fully reflects the company's research and development strength and marketing channels.

|

Source: Calculated based on the company's 2016 annual report data

2.3 Summary

In 2006, Shijiazhuang Group's revenue contribution from innovative medicines accounted for about 40%, of which NBP's contribution revenue accounted for more than 20%, and single product profit contributed more than 40%. The company's core variety, NBP, still has huge market space, and the future space is expected to reach 5 billion. The cardiovascular and anti-tumor fields are the two largest areas in the Chinese pharmaceutical market. The company has a strong layout in the cardiovascular and cerebrovascular fields, and has made positive progress in the anti-tumor field. The product echelon is reasonable and its advantages are expected to continue.

The current sales revenue of Hengrui Medicine is still mainly contributed by generic drugs, and the revenue of innovative drugs accounts for about 10% of the receivables. With the approval of a number of new drugs from the company in 2018 and 2019, it is expected that the company's new drug revenue contribution will increase after 2019. Hengrui's various generic products are technically difficult, the market is large, and with a strong marketing team, under the two-wheel drive of generic drugs and innovative drugs, the company will usher in a new phase after 2019-2020. The period of rapid growth.

3. R&D and reserve comparison

As a representative enterprise of innovative Chinese medicines, Shijiazhuang Group and Hengrui Medicine have hundreds of innovative medicines and generic drugs. The two companies have detailed research varieties and market prospects. The major brokers have already had a lot of analysis. They are not listed here. Only a few important varieties are briefly analyzed.

3.1 Shijiazhuang Group

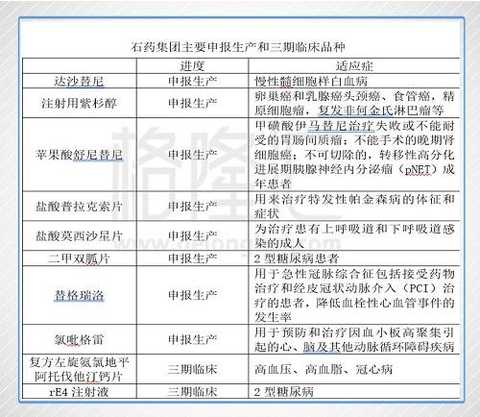

In the first half of 2017, the company is researching more than 170 new products, mainly in the fields of cardiovascular and cerebrovascular, diabetes, anti-tumor, psychology and anti-infection. Among them, there are 18 new drugs and 49 new drugs. The Group submitted a total of 4 clinical applications and 5 production applications to the State Food and Drug Administration. The company has 32 products pending approval in the State Food and Drug Administration.

|

Source: company annual report, announcement

As can be seen from the above table, the company has heavy varieties in the fields of anti-tumor, cardiovascular and cerebrovascular diseases and diabetes. In anti-tumor, the company's first small-molecule targeted drug, Nolin, was approved for marketing in 2015, and sunitinib malate and dasatinib have also been declared for production, plus the upcoming paclitaxel for injection, the company In the field of anti-tumor, the strength is greatly strengthened; in the cardiovascular and cerebrovascular aspects, clopidogrel and ticagrelor are mainly used for anticoagulation after PCI. The domestic market scale is more than 10 billion, and the competition pattern is good; in the field of diabetes, metformin Tablets and metformin sustained-release tablets have also been declared for production. The biological class 1 innovative drug GLP-1 analogue rE4 injection is in clinical phase III and is expected to be approved in 2019.

In terms of R&D expenditure, compared with other domestic pharmaceutical companies, the absolute amount of R&D investment and the proportion of R&D investment in revenue are not high. For example, China Biopharma's 2016 R&D investment is 1.599 billion Hong Kong dollars (more than 1 billion). RMB), 1.94 billion yuan of Hengrui Medicine, 600196 of Fosun Pharma, and 1.106 billion yuan of shares. The R&D investment of Hengrui Medicine and China Biopharmaceuticals accounted for more than 10% of the revenue. The intensity of R&D investment is indispensable for building long-term competitive advantage. Shijiazhuang Group needs to further strengthen R&D investment.

|

Source: The company's 2016 annual report, executive disclosure and calculations

3.2 Hengrui Medicine

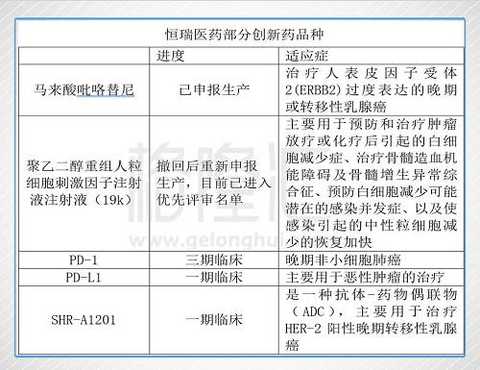

After years of research and development investment, the company has stocked a large number of new drug varieties, including pre-clinical, research and production. In the first half of 2017, the company invested 780 million yuan in research and development, a year-on-year increase of 60%. From 2015 to the first half of 2017, only 34 clinical patents were submitted, and more than 60 generic approvals and production approvals were issued. The abundant reserve products provided a solid guarantee for the company's future development.

|

Source: company annual report, announcement and network

In 2015, the company's PD-1 project SHR-1210 was licensed to US Incyte before it was listed, with a revenue of $25 million plus a total of 770 million US dollars. At present, the project has been suspended by overseas partner Incyte, but domestic clinical trials are still continuing and it is expected to become the first domestically produced product.

On August 24, 2017, the application of pyrrolidine maleate was approved by CDE and entered the approval process. Pyrrolidine is a 1.1 class EGFR/HER2 inhibitor independently developed by Hengrui for the treatment of HER2-positive metastatic breast cancer. It is expected that the company will become 1.5 billion to 2 billion after the product is launched.

19K: Tumor chemotherapy usually kills normal cells or causes bone marrow suppression, resulting in a significant reduction in white blood cells, increasing the risk of fever or infection in patients. It is generally necessary to use whitening drugs to increase the number of white blood cells in patients and to obtain the ability to resist complications of chemotherapy infection. Considering the trend of long-acting G-CSF replacing short-acting G-CSF, and Hengrui's clinical data is significantly better than competing products, relying on strong sales capabilities, it is expected to become a potential product of more than 1 billion products.

In terms of R&D expenditure, Hengrui Medicine is one of the most intensive enterprises in China, and it maintains a revenue of around 10%. Hengrui Medicine has established the most powerful R&D team in China with more than 2,000 employees. Hengrui Medicine will fully expense research and development expenses.

|

Source of data: company annual report and calculated income

Fourth, the company's development path comparison

4.1 Shijiazhuang Group

In 1938, Shijiazhuang Yizhi Group, one of the predecessors of Shijiazhuang, was established and was one of the earliest pharmaceutical companies established by the People's Liberation Army.

In 1994, its holding subsidiary, China Pharmaceutical (1093.HK), was listed on the main board of Hong Kong and became the first pharmaceutical company listed in Hong Kong.

In August 1997, it was jointly established by Hebei Pharmaceutical Group, Shijiazhuang Yipiao Group, Shijiazhuang Second Pharmaceutical Group and Shijiazhuang Four Medicine Co., Ltd.

In 1999, Shijiazhuang Group bought 50 million yuan of the patent for the new class of national medicine NXP from the Chinese Academy of Medical Sciences.

On September 30, 2002, Shijiazhuang obtained the production approval and new drug certificate for the new class of national drug “butyl benzoquinone†with independent intellectual property rights.

In 2003, in order to realize the industrialization of butylphthalide, 380 million yuan was invested in the construction of the stone medicine group NBP.

On June 16, 2007, Legend Holdings and Shijiazhuang State-owned Assets Supervision and Administration Commission formally signed a property rights transfer agreement to acquire 100% of the state-owned property rights of Shijiazhuang Group at a price of 870 million yuan.

On April 14, 2010, butylphthalide sodium chloride injection obtained new drug certificate and registration approval.

In 2011, Jin Youli won the new drug certificate and started the fourth phase clinical research in 2012. It is the first long-acting whitening drug approved in China.

On June 27, 2012, China National Pharmaceutical Group announced that it will issue an additional HK$8.98 billion to acquire the pharmaceutical manufacturing and sales business to major shareholder Hony, and renamed it Shijiazhuang Group.

At the end of 2012, the clopidogrel hydrogen sulfate film tablets and penicillin G potassium produced by Shijiazhuang Group passed the US Food and Drug Administration (FDA) certification.

In 2013, Hony Capital gradually sold shares in Shijiazhuang and sold them in 2015. After the transaction was completed, the company's chairman and CEO Cai Dongchen became the actual controller, with a shareholding ratio of approximately 30%.

In 2015, Nolin was approved for marketing and was the company's first approved small molecule targeted drug.

Since the establishment of the four pharmaceutical companies in 1997, the Shijiazhuang Group has been at the forefront of the country. In 2003, its revenue and total profit were ranked first in the industry. It can be said that the starting point is relatively high. Therefore, the key to the development of Shijiazhuang Group is not the scale problem, but how to adjust the product structure, that is, from raw material medicine to general medicine to innovative medicine. Among them, in 1999, it spent huge sums of money to purchase butylphthalide patents in the company. The most important role played in the transformation process.

The promotion of NBP is not smooth at the beginning of the listing. The sales amount of the listed company was only over 3 million in the same year. It has suffered losses for four consecutive years. By 2008, the accumulated loss was 100 million yuan, and the pharmaceutical company’s investment in NBP has reached 450 million. Yuan, Cai Dongchen is facing tremendous pressure. Under such circumstances, Shijiazhuang Group insisted on the use of academic promotion to conduct new drug marketing, which is common to international giants in promoting new drugs, while domestic counterparts are less used. In the fifth year of the listing of NBP, the sales exceeded 500 million yuan, the sales in 2016 exceeded 2.5 billion, and the profit of single products exceeded 1 billion. Participated in the research, clinical and marketing of butylphthalide, laying a good foundation for the complete R&D, production and sales system of Shijiazhuang Group, and established a domestic first-class R&D team, which made Shijiazhuang Group Stepping into the ranks of the most innovative pharmaceutical companies in China.

The Group's correct judgment on the future development trend of the pharmaceutical industry has taken the road of technology-driven. As the largest raw material drug production base in the country at that time, the company's efficiency was at the forefront of the country, but the Group realized that such a situation is not sustainable and technological innovation can guarantee long-term development. In addition to maintaining its advantages in the cardiovascular field, the Shijiazhuang Group has made great progress in the fields of anti-tumor, diabetes and psychology. In addition, the completion of the restructuring of the group made the management's interests closely integrated with the development of the company. The enthusiasm of the management was stimulated, the new products were listed one after another, and the product structure was optimized.

4.2 Hengrui Medicine

In 1970, the Lianyungang Pharmaceutical Factory, the predecessor of Hengrui Medicine, was established, and its main business was the processing of APIs.

In 1990, Sun Feiyang became the factory manager. The book profit of the company was only 80,000 yuan. The products were single, aging, and the added value was low, on the verge of bankruptcy.

In 1992, with the company's profit limited, Sun Feiyang decided to take out 1.2 million yuan to go to the Beijing research institute to buy the new drug ifosfamide. In 1995, the drug was successfully listed, and the sales of single products exceeded 10 million.

From 1991 to 1996, Hengrui Pharmaceutical developed more than 20 new products, and the company entered a track of sound development. In 1996, its sales revenue exceeded 100 million yuan.

In 1996, Hengrui invested more than 20 million yuan to build more than 3,000 square meters of Lianyungang R & D center into use. Emphasis on research and development has become the consensus of the company.

In 1998, the company began to develop oxaliplatin generic drugs. In 2001, it successfully went into production and became the first imitation. In 2002, it achieved sales of more than 80 million yuan. In 2005, its sales revenue was nearly 300 million yuan.

In 2000, it was listed on the Shanghai Stock Exchange of Hengrui Medicine, raising 460 million yuan.

In 2000, Hengrui invested 180 million yuan to build an international standard laboratory of 10,000 square meters in Shanghai, and determined the development of anti-tumor drugs, cardiovascular drugs, anesthesia analgesics, surgical drugs, and prevention of common diseases and frequently-occurring drugs. The scientific research strategy, taking more than 8% of the total sales each year as research funding, and quickly transforming into innovative pharmaceutical companies.

In 2003, the company first appeared in Docetaxel, and the price was only one-third of the import. The original researcher Sanofi's Docetaxel entered the Chinese market around 2002. Sanofi-Aventis sued with Hengrui’s alleged patent infringement of the patented “Docetaxel†raw material. The lawsuit ended with Hengrui’s victory.

In 2005, Hengrui invested US$3 million to build an overseas research institute in San Francisco, USA, to conduct innovative drug research and development, and to track the most cutting-edge information on world drug research.

In October 2006, Hengrui USA was established in New Jersey and set up two laboratories specializing in new drug innovation research, and assisted in FDA filing and drug registration.

In May 2010, Zhang Lianshan joined Hengrui Medicine and became the company's deputy general manager and global research and development president.

In 2011, Hengrui's new class 1.1 drug, Ayrexib, obtained the production approval, which is Hengrui's first innovative drug. Ericsson's research and development work began in 1999 and lasted nearly 12 years.

On December 17, 2011, irinotecan injection produced by Hengrui passed the FDA certification inspection. The road to internationalization of Hengrui Pharmaceutical Products was opened.

In November 2014, the 1.1 new drug apatinib tablets independently developed by Hengrui Medicine were approved for production. Apatinib lasted for ten years from the development of the project to the approval of the listing. In 2017, the sales of this variety is expected to exceed 1 billion.

On September 3, 2015, Hengrui announced that the company's PD-1 project SHR-1210 had a license to the US company Incy before it was listed, with a revenue of US$25 million plus a total mileage of US$770 million.

On August 24th, 2017, the application for the listing of Hengrui Pharmaceutical Pyrrolidine Tablets was obtained by CDE and entered the approval process. Pyrrolidine is a 1.1 class EGFR/HER2 inhibitor independently developed by Hengrui for the treatment of HER2-positive metastatic breast cancer. It is expected that the variety will become a heavyweight with sales exceeding 1 billion after its launch.

From the above development track, we can clearly see how Hengrui has grown from an ordinary pharmaceutical factory to a leader in innovative Chinese medicine. With the advanced thinking and market acumen, Sun Feiyang selected the most promising market segment, the anti-tumor field, and invested heavily in the rapid introduction of cyclophosphamide, oxaliplatin, docetaxel and other varieties. The company recognized the importance of R&D earlier. After having the financial strength and certain technical accumulation, it invested heavily to establish a first-class R&D center in China and upgrade its technical strength. With the completion of the listing and corporate restructuring, Hengrui is completely privatized, stimulating the enthusiasm of the management, constantly launching a series of heavy varieties, and establishing advantages in the fields of surgical anesthesia and contrast agents, achieving sales and research and development go hand in hand.

Hengrui's innovation system is basically complete, with a group of first-class scientists with international vision, such as Zhang Lianshan, and the rapid approval of innovative drugs and the rapid development of internationalization, which provides a strong impetus for the company's future growth. . Hengrui's future development is extremely clear, and it is only a matter of time before it becomes a world-class pharmaceutical company.

4.3 Summary

There are many similarities between the Shijiazhuang Group and the Hengrui Medicine Development Path.

First of all, both of them have strong corporate leaders who have the courage to seize opportunities at key moments. For example, Cai Dongchen took out nearly half of the company’s profits to purchase the “butyl benzophenone†patent, and Sun Feiyang paid heavily for the purchase of “cyclophosphamideâ€. The foundation in the field of cardiovascular and anti-tumor. The success of innovative drugs or difficult generics has enabled companies to establish a high standard of R&D, production, quality control, marketing systems and high-level teams. The lucrative profits brought by the new drugs will also strongly support the continuous research and development of enterprises, thus forming a virtuous circle.

Secondly, the forward thinking and firm determination of enterprises to transform into innovative pharmaceutical companies. At the beginning of the development of the two, the main business was basically raw materials and generic drugs, with low added value and unsustainable. The two have determined that innovation is the development direction of the enterprise, investing heavily in establishing R&D centers, attracting talents, and leading most of their peers for more than 5-10 years, thus building a strong competitive advantage.

Third, the enterprise is reformed and the management achieves control. With the special background of the times and favorable timing, the two realized the management holding through the share-trading reform and the state-owned equity transfer. The success of the restructuring has made management interests and corporate interests consistent, and the company's development has entered a period of rapid growth.

Fourth, under the premise of ensuring the advantages of the original field, actively expand to other areas and create new growth points. In the cardiovascular field, Shijiazhuang Group has launched Xuan Ning, a heavy medicine, and has risen strongly in the field of anti-tumor. It has launched Jin Youli, Duomei and small molecule targeting drug Nuolining, and together with NBP to form stone medicine. New drug cluster. In the case of the strong consolidation of the anti-tumor field, Hengrui has created surgical anesthesia, contrast agents, etc., and has a large number of product ladders of 500 million to 1.5 billion.

Fifth, the new drug has been accelerated and approved. At present, the number of new drugs being researched and will be approved for production is accelerating. The suntan's sunitinib and dasatinib have also been declared for production. The soon-to-be approved paclitaxel for injection and the bio-class 1 innovative drug GLP-1 analogue rE4 injection are in the third phase of clinical, all of which are large varieties; Rui's pyrrolidine, polyethylene glycol recombinant human granulocyte stimulating factor injection, and paclitaxel for injection have all been reported, and PD-1 monoclonal antibody is in clinical phase III. It is expected that a new round will be opened from 2019 to 2020. In the period of rapid growth, the real innovation drug is promoted.

Sixth, international progress has made positive progress. At present, 6 medicines have been approved by the FDA, and 4 medicines have been filed with ANDA. In Hengrui medicine, atracurium, acetophenone acetate, cyclophosphamide, and sevoflurane for inhalation have been successfully realized. Overseas Sales. There are many forms of internationalization, and the export of preparations is only one aspect. The overseas clinical, overseas joint development, overseas patent authorization, introduction of overseas products and future international mergers and acquisitions of new drugs are all available for future internationalization.

V. Comparison of the hidden dangers faced by the two

5.1 Shijiazhuang Group

After the reorganization of Shijiazhuang Group, Cai Dongchen became the actual controller of the company, and the shareholding ratio was close to 30%. The shareholding ratio of other shareholders was low, and there was no worry about the company's control. The main problems facing the Shijiazhuang Group are concentrated at the business level.

5.1.1 Biopharmaceutical layout is late

In 2014, among the top 100 drugs with the highest global sales, the number of biological products has reached 44, and the sales of biological products accounted for 23% of the total sales of the pharmaceutical market. It is expected that this proportion will rise to 2020. 30%. The research and development of biomacromolecules, especially antibody drugs, has become a hot spot in the development of new drugs worldwide. The Shijiazhuang Group has obvious advantages in chemical medicine. In recent years, it has also actively deployed in biopharmaceuticals. Shijiao currently has biological research laboratories in four cities: California, Texas, Boston, and Princeton. Although there are some listed and research products, they are lagging behind the domestic giants such as Hengrui.

5.1.2 Core variety butylphthalide (NBP) patent expiration problem

Shijiazhuang Group butylphthalide capsule expires in 2023, and the number of injection patents expires in 2022, but Shijiao Group does not have a compound patent for butylphthalide. The patent for this compound for acute ischemic stroke will also be 2019. maturity. In order to extend the life cycle of this product, Shijiazhuang Group has also applied for patents for the new indications of butylphthalide, levothinobenzoquinone, and butylphthalide related substances.

In March 2017, Nanjing Youke has submitted four types of imitation applications for butylphthalide bulk drugs and 2.2 new drug registration applications for butylphthalide injection. Lizhu is also applying for the clinical trial of butylphthalide injection.

5.1.3 Raw material drug business problem

The company's API business is mainly composed of antibiotics, vitamin C and caffeine, contributing about a quarter of the group's revenue. One of the risks faced by the API business is environmental protection, and the Shijiao Group is located in a heavily polluted area of ​​the North China Plain, closer to Beijing and more susceptible to environmental protection policies. In the long run, retaining the larger-scale API business is not in line with the strategy of the Shijiazhuang Group. In order to become an innovative pharmaceutical company at home and abroad, and focusing on innovative medicines and high-end preparations, Shijiazhuang Group must concentrate resources and reduce or split the raw material medicine business. At present, the company has made clear plans for the API business and implemented it according to the plan.

5.2 Hengrui Medicine

Compared with the hidden dangers faced by Shijiazhuang Group, Hengrui's business base is relatively solid. No matter the existing product line, reserve R&D and sales, there is no obvious shortcoming. The main worry of Hengrui Medicine is external.

5.2.1 Horizontal competition with Hausen Pharmaceuticals

Hengrui needs to resolve the competitive relationship with Haosen Pharmaceutical. The head of Haosen Medicine is Zhong Huijuan, who is a husband and wife relationship with Sun Feiyang. The two companies have a high degree of overlap in the business line, especially in the field of anti-tumor. In 2008, Sun Feiyang publicly stated that Howson Medical will be acquired by Hengrui Medicine, but this has not happened. In the past few years, it has been reported that Haosen Pharmaceutical will be listed on Hong Kong stocks. Surprisingly, in the face of the phenomenon of horizontal competition between the two companies, the CSRC and relevant departments have not had any questions. There should be reasons for outsiders not knowing.

5.2.2 The worry of enterprise control

Jiangsu Hengrui Group holds 24.31% of the equity of Hengrui Medicine, and Sun Feiyang holds 89.22% of the equity of Hengrui Pharmaceutical Group. Although it is the actual controller of the listed company, the shareholding ratio is not high, which is also the less There is one reason for the large capital operation. Dayuan Investment currently holds 15.84%, second only to Hengrui Pharmaceutical Group. It is relatively mysterious. It is rumored that the company is actually controlled by Sun Feiyang, but the Hengrui Medical Annual Report disclosed the two non-coherent actors. Other shareholders, China Pharmaceutical Investment Co., Ltd. and Lianyungang Financial Holding Group are state-owned legal persons. China Securities and China Central Securities are also state-owned. The shareholding ratio of Hong Kong funds is 11.10%. It is not known whether the multi-party is playing a fierce game behind the equity of China's highest quality and most innovative pharmaceutical companies.

|

Source: Hengrui Medicine 2017 Semi-annual Report

Conclusion

As a representative enterprise of China's pharmaceutical industry, Shijiazhuang Group and Hengrui Medicine rely on flexible management system, actual control of people's vision, advanced strategic vision, practical strategic planning, continuous large-scale R&D investment, and good product echelon. With a significant advantage in the segmentation area, it is foreseeable that the two will move forward steadily and successfully enter the ranks of innovative pharmaceutical companies in China and the world.

Pharmaceutical R&D and manufacturing is a conscience project. It needs to focus, accumulate and resist all kinds of temptations to make quick money. The research and development of innovative drugs is facing long-term high risks. I sincerely hope that Chinese pharmaceutical leaders can walk in the tide of great health. More stable and farther.

LSR Injection Molding and Silicone Injection Molding

LIM & LSR Molding, also known as LSR & Liquid Silicone Rubber Molding and LSR Injection Molding (LIM) & Silicone Injection Molding, is a process to pump the high purity platinum cured silicone (supplied in barrels: A + B components at 1:1) through a static mixer for into the heated cavity and vulcanized, which is suitable for the production requiring high quality, high precision and high volume.

LIM & LSR Molding is typically applied for sealing membranes, electronics, infant products, medical products and overmolded products, etc.

Lsr Injection Molding ,Silicone Injection Molding ,Liquid Silicone Injection Mold,Silicone Injection Mold For Medical

Xiamen The Answers Trade Co.,Ltd. , https://www.xmanswerssilicone.com