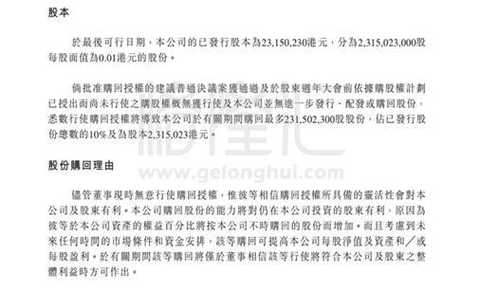

▌ Accelerated repo

On April 20, 2017, Huadi International Holdings announced the announcement of the general meeting of shareholders, claiming that it will repurchase up to 23,150,230 shares during the year. At that time, the total share capital of Huadi was 231,502,300 shares, which is exactly 10% of the shares of Huadi. The reason for the repurchase in the announcement is relatively common, mainly indicating that the repurchase behavior has reduced the share capital, which is beneficial to the shareholders who still invest in Huadi. At the same time to improve the net value per share and earnings per share, the purpose is nothing more than to improve the company's market valuation, the company's share price has a certain boost.

China Land was listed on the Hong Kong Stock Exchange in 2010 and its initial issue price was HK$5.93 per share. Shortly thereafter, it entered a continuous downward trend, and today the stock price is 1.66 Hong Kong dollars per share. Therefore, the second reason mentioned above is somewhat insignificant.

From this point of view, the main purpose of Huadi repurchase is to increase the shareholding ratio of the original shareholders by reducing the tradable share capital. There is no doubt that the biggest beneficiary is definitely the company's major shareholder.

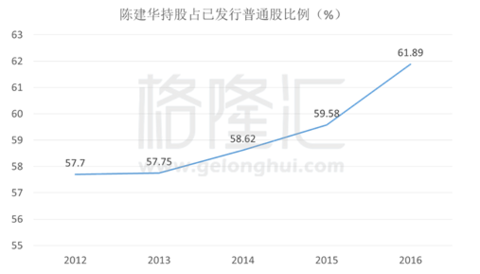

Since 2017, there has been no major shareholder change in China. We can see the current shareholding of the company through the major shareholders' equity disclosed in the 2016 Annual Report of China:

The largest shareholder, Octopus Holdings Foundation, currently has about 1.44 billion shares of common stock, accounting for 61.89% of the total share capital. The founder of the group, Chen Jianhua, is the sole shareholder of the Octopus Holdings Foundation and is therefore regarded as the largest controlling shareholder of China. At present, Chen Jianhua is responsible for the overall strategic planning for the chairman of the company's board of directors.

The second largest shareholder is a foreign investment institution of International Value Advisers, LLC. The institution invested in China in 14 years and held approximately 1.31 billion shares, accounting for 5.31% of the company's third largest shareholder. At the time, Matthews International Capital Management, LLC, the second largest shareholder, held 1.77 billion shares, accounting for 7.17%, and withdrew in 2015. In the same year, International Value Advisers, LLC increased its holdings of 1.32 billion shares to become the second largest shareholder, and there has been no significant change in its holdings so far.

The largest shareholder is also very low-key. Since 2012, Chen Jianhua’s shareholding has remained unchanged, and there have been no initiatives that have attracted market attention. However, its shareholding ratio has been quietly rising.

In the absence of any increase in holdings, Chen Jianhua's shareholdings remain unchanged, but there is only one reason for the increase in the proportion of holdings, that is, the company has repurchased. As early as 2013, Huadi had repurchased its shares, but at that time it repurchased 0.08% of its share capital. The actual start of the obvious repurchase is from 14 years, and the number of shares repurchased in 14 and 15 years accounted for 1.49% and 1.61% respectively. After entering 2016, there was a significant acceleration. In the 16 years, the proportion of repurchase in the whole year was 3.73%, up 131.4% year-on-year. The following is the situation of Huadi repurchase from 2012 to 2017:

In 17 years, the company did not slow down the pace of repurchase. As of May 10, the company repurchased 6,178,700 shares, accounting for 0.88%, compared with 0.26% in the same period last year. As of 2016, Huadi has repurchased nearly 7% of its equity. It is expected that the repurchase of China will be greater in the future, and the proportion of major shareholder holdings will accelerate.

Under normal circumstances, the company made a large-scale repurchase, showing that the management and shareholders of the company are very optimistic about the company's expectations, and that the stock price is undervalued by the market. Then we will analyze how the business operations of China Land in recent years.

▌ depressed department store

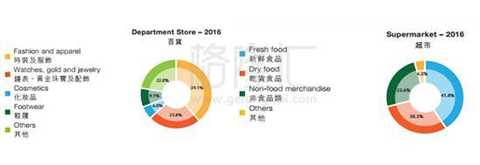

Huadi operates department stores and supermarkets in China, and the three core brands “Yaohanâ€, “Huadi Department Store†and “Dongtonghua†supermarkets are mainly engaged in the middle and high-end consumer markets of third- and fourth-tier cities. To put it simply, Huadi's main business is two department stores and supermarkets. The difference between the two is mainly that the things sold are different. The figure below clearly shows the difference in the merchandise between the department store and the supermarket in Huadi.

Huadi Department Store and Supermarket mainly have three profit models: independent retail, joint sales, and counter rental. Self-sales retail is to sell and sell their own products in department stores or supermarkets; joint sales is to assist other brands to sell proportionately to earn commissions; counters are rented directly to other brands or companies to earn rent.

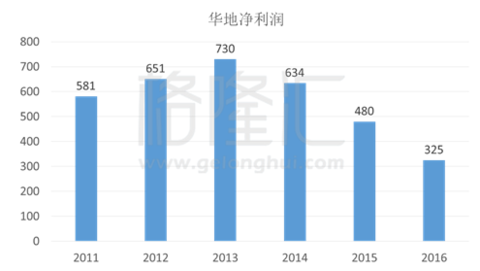

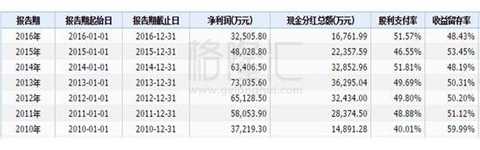

The following is the net profit of Huadi in the past 6 years. It can be seen that the situation of business operations is very difficult, and it has continued to decline in 13 years.

In fact, it is not just Huadi. As for the entire retail industry, the profit decline in recent years has been very serious. The “closed shop tide†that has started in 15 years has not stopped. In 2015, China's department store closed stores in 17 provinces and autonomous regions, 14 brands, and 63 department stores. In 2016, 22 companies closed 41 stores in individual department stores, shopping malls and large supermarkets of over 2,000 square meters.

Huadi's annual operating income is actually very stable. In 2016, its operating income was 4.19 billion yuan, almost the same as last year. Therefore, from the recent operating expenses of China, we can sum up the reasons for the decline in profits:

1. Domestic labor costs are getting higher and higher , and department stores need to expand and maintain the retail network, which requires a large number of sales personnel, and labor shortages further increase costs.

2. Under the impact of Internet e-commerce, the industry accelerated the reshuffle . In order to continue to expand into high-quality locations for development, Huadi needs to renovate stores, etc., which will increase the depreciation and amortization of fixed assets every year, thereby increasing costs.

3. Other expenses have risen , mainly because more water, electricity, and miscellaneous fees are needed for continued expansion, and various expenses and taxes have risen. In addition to this, other expenditures increased significantly in the past 16 years, as Huadi closed Nanjing's Yaohan Department Store for full goodwill impairment.

Huadi and the entire industry began to show a significant decline after 13 years, and it happened that the company began to repurchase from this time, and continued to increase repurchase in 17 years. There are two possibilities here. One is that corporate executives and shareholders have made serious mistakes, and they are “faced†every year. The other is that companies believe that the current stock price is seriously undervalued. The second possibility is significantly larger, so we need to see if Huadi is currently undervalued by the market.

▌ underrated Haiti

Unlike other companies in the industry that operate department stores, Huadi’s properties are owned by most of its department stores. From the above-mentioned map of China's operating expenses, the proportion of rental expenses in the overall cost is also very small. The 16-year rent only accounts for 5% of the overall cost, accounting for 0.9% of the total sales proceeds. Therefore, we can analyze the valuation of the company through PB.

As shown in the above figure, in 2015, the PB of Huadi officially fell below 1, while the PB of 16 years reached 0.5. The net assets per share increased year by year, so the PB continued to fall because of the decline in stock prices.

The PB of 0.5 shows that if the stock price does not change, we can buy the whole company with the cost of half of the net assets of China, which is undoubtedly underestimated. Of course, under this valuation, the market is also extremely optimistic about the future of the company. The PB of 0.5 also means that the market believes that China will have a large loss in the future, resulting in a net depreciation of half of the net assets. But this view is obviously unreasonable.

As can be seen from the above chart, Huadi's revenue is quite stable. In the process of PB's continued decline, the company's net assets have kept rising. Although China's profits continued to decline, it remained positive and did not suffer losses.

The reason for the decline in profits is mostly due to the increase in costs due to the transformation and continued expansion of Huadi stores. Therefore, a large part of the actual income has already flowed into the net assets of the company, and the growth of the corresponding enterprises has also been improved.

The net cash flow from operating activities continued to rise and operational capacity improved. In addition, the annual dividend payment rate of Huadi is maintained at around 50% per year, and the overall cash is sufficient.

We also evaluate the situation in the industry at the same time:

It can be seen from the industry data that since 2013, the retail sales growth rate of retail enterprises has fallen to a close in 1 year, and the whole industry has entered negative growth since 14 years. After several years of bankruptcy and mergers, the sales growth rate continued to rise after the end of the 16th year.

Therefore, the possibility of a large loss in the future of China is not high, and the current stock price is indeed seriously underestimated.

The market value of the company has been seriously underestimated to provide confidence in the repurchase of China, and now it seems that the accelerated repurchase has also stepped in the market turning point. If you do not perish in silence, it will erupt in silence. For so long, the major shareholder has increased the shareholding ratio through the silent repurchase of the company, and then there is a high probability that further action will be taken.

Then let's guess what "big moves" will happen in China in the future, and we can get some investment opportunities based on speculation.

▌ next three guess:

Guess one: Selling assets to improve performance

Huadi's department stores and supermarkets are held in the form of holding subsidiaries. When the subsidiaries are officially completed, they will form a book value, while properties and buildings are accounted for as fixed assets. The annual report also shows that the book value of all department stores and supermarkets remains unchanged. After the property is included in the fixed assets, it is depreciated every year by depreciation, while the property market price is appreciated.

Huadi's department stores and supermarkets are mainly distributed in Anhui, Zhejiang and Jiangsu. The earliest department stores were registered in 1993. From 2002 to 2015, the appreciation of the property was about 2-3 times. This part of the appreciation is not reflected in the book value of Huadi, only when it is sold, it will be calculated based on market value and released.

At this time, Huadi has increased its repurchase. We can reasonably speculate that the major shareholder must have the desire to increase the company's profits and re-do the market value of large enterprises. By closing stores with low profit margins and selling undervalued properties, it will bring a lot of profits. Improve business performance and reduce the cost of depreciation. At the same time, cash is recovered to support enterprise transformation and expansion.

We can make a vague estimate of how much profit a company will generate if it sells its assets. Huadi's annual report shows that 19 department stores have a total area of ​​1.01 million square meters, and 51 supermarkets have a construction area of ​​441,000 square meters. Among them, 914,000 square meters of department stores are self-owned properties, so it is estimated that 90% of the total property area is 1.451 million square meters. The average property market price of the three places is now around 10,000 yuan, which can be used to vaguely estimate the value of the total self-owned property to be 13.17 billion.

The fixed assets of property and construction on the books totaled 8.77 billion, which was reduced as a cost when the property was sold. Without considering the tax expenses, the final result is that the profit margin of each 1 square meter of self-owned property can be more than 50%, while the gross profit margin of Huadi in 16 years is only 12%.

If the future of China really sells assets, what is the performance of its stock price? Here we can refer to an example that is also a department store: Parkson Group.

Parkson is the first foreign department store to enter the Chinese market. After 2012, following the industry downhill, and even began to lose money in 15 years, the stock price has been falling, and it is terrible. The stock price fell from a total of 8 Hong Kong dollars per share in 12 years to a minimum of 6 cents per share in August, a drop of 92%.

Surprisingly, on September 14, 2016, Parkson announced the sale of Beijing's loss-making property Sun Palace Parkson. The net proceeds from the sale of this asset are about 1.9 billion, and the expected revenue is 900 million yuan. In the first three quarters of 2016, Parkson’s revenue was 3.4 billion yuan and the net profit was 250 million.

Parkson's share price jumped nearly 40%, once more than 68% reached around 1.08 yuan, and then the repair market reached a minimum of 0.7 yuan. Since then, it has continued to rise, and the latest price has returned to 1.08 yuan.

If Huadi sells property assets, there is a good chance that a similar market will occur. If the performance is improved, there will be medium and long-term investment opportunities.

Conjecture 2: Privatization delisting

The privatization of enterprises to delist is in fact the major shareholder through the tender offer to acquire the shares of other shareholders in the market to achieve full control, and then delisted. The factors that reflect the privatization of China are as follows:

1. Long-term underestimation is not conducive to corporate financing. Huadi's share price has been lower than the IPO issue price after 11 years. In terms of the PB analyzed before, the current PB is 0.5. If the financing is based on this valuation level, the enterprise assets worth 1 yuan can only be melted to 0.5 yuan, and directly hit 50%. A serious underestimation will lead to an increase in corporate financing costs.

2. The trading volume of the stock is small, and the transaction is too light, which affects the liquidity of the stock. The average daily turnover of Huadi in the past 52 weeks was 2.76 million yuan, and the average daily market capitalization was 2.9 billion, accounting for less than 0.1%. The average daily turnover rate is only about 0.1%.

3. The shareholding structure is very concentrated. The shareholding ratio of the major shareholder Chen Jianhua reached 61.89%, and the repurchase will continue to further concentrate the shareholders' equity. Not only helps to reduce the cost of the company's privatization, but also greatly increases the possibility of successfully passing the shareholders' meeting. Huadi quietly repurchased its share capital, which can be understood as a major shareholder’s use of corporate funds to purchase assets in disguise. Today, the share of stocks in the hands of non-large shareholders of China is less than 30%.

4. Maintain a high dividend payout ratio. Since its launch, Huadi has been paying dividends of 50% of cash, which is close to the net profit every year, even after 13 years, the profit has been falling. To be good, this is very friendly to investors. From a bad perspective, this reflects the “cash-out†behavior of major shareholders to the company and prepares for the next acquisition of the company.

Then, if there is privatization in the future, there will be a situation in the stock price. Here, take the "peer" business as a reference example.

Wumart Commercial was listed on the Growth Enterprise Market of the Hong Kong Stock Exchange at a price of HK$6.22 per share in 2003 and transferred to the Main Board of Hong Kong in 2010. On October 20, 2015, Wumart Commercial, which was suspended for two weeks, announced that it will make a voluntary conditional offer for H shares and domestic shares. If implemented, this will cause Wumart to withdraw from the market. The company gave an offer price of HK$6.22 per share, which is more than 90% higher than the 3.27 Hong Kong dollar before the suspension.

If Huadi is privatized, major shareholders will need to acquire equity. We can assume that the current shareholding structure and stock price remain unchanged, and estimate how much premium space the company can provide to major shareholders. Today, the total share capital is 2.315 billion shares, and the stock price is 1.65 yuan per share. Then 30% of the market value of the market is 1.13 billion, which is counted as the lowest acquisition cost.

Regardless of the undervalued property, the major shareholder will sell the net assets of the acquired company at a book value of 5.14 billion, so the difference from the minimum acquisition cost is about 2 billion. It is further estimated that the maximum premium payable per share is about 2.9 yuan per share, and the maximum premium space is about 176%.

If privatization needs to meet two conditions: 1 at least 75% of the voting rights of the non-interested shareholders (independent shareholders) attending the meeting will be voted for; 2 the votes of the voting against the resolution shall not exceed the voting rights of all uninterested shares. 10%. Therefore, in order to take into account the interests of other shareholders, the acquirer usually needs a premium to acquire the equity, which will certainly result in a stock market similar to the above example.

Conjecture 3: Inclusion of the MSCI Index

On May 16, 2017, in the MSCI announcement, Huadi was included in the China Small Cap Index. Effective after the market closes on May 31. MSCI is the world's number one index compiler, with a total of more than $10 trillion in funds linked to its index products. In other words, once a country's stock is included in the MSCI benchmark stock index, it will bring a very large amount of global investment to the market.

The international index funds linked to the MSCI index are some passive index funds, and the funds will be distributed to the constituents of the MSCI index. The annual adjustment will be completed on May 31. On the day of the adjustment of the constituent stocks, these passive funds will adjust the investment targets accordingly, reduce the stocks of the listed companies, and buy new ones. On the same day, it may generate a large volume in the stock.

We can analyze the performance of the Hong Kong stocks that were included in the index on the day of May 31 when the MSCI China Small Cap Index was adjusted in the previous year. Take a look at how it affects corporate stocks. On May 13, 2016, 30 Hong Kong stocks were announced to be included in the China Small Cap Index. We take a time-sharing chart of the three stocks with the largest amplitude on May 31 for analysis.

China Heart Connected Fertilizer: The maximum amplitude of the day was 17.4%, closing at -2.27%

Huili Resources: The maximum amplitude of the day was 16.25%, an increase of 13.79%.

Guoxin Real Estate: The maximum amplitude of the day was 12.66%, an increase of 7.43%

Obviously, these stocks have a very large volume at the end of the day, causing the stock price to rise rapidly. But before or after the day, or after a few days, the stock price has retreated to a new level. The average price of 30 stocks on May 31 was 2%, and the average amplitude was 6%. It is obvious that there are not many stocks with obvious influence. Among them, there are 10 stocks with more than 7% amplitude and obvious trading opportunities, accounting for 30% of the total. .

Therefore, China Land was confirmed to be included in the MSCI China Small Cap Index, and a similar market may appear on May 31.

▌ Summary:

Warner International Holdings has been in a downturn in the commercial department store industry, and corporate shareholders have been underperforming for a long time. At present, the stock price has been undervalued, and the recent accelerated repurchase of the company indicates that there will be further positive actions in the future. We thus guess the three "big moves" that will happen in the future. First, in the future, it is highly probable that China will improve its performance by selling undervalued properties. Second, if the valuation cannot be improved, the largest shareholder, Chen Jianhua, is likely to privatize and delist from China. Third, the recent determination of China to determine the inclusion of the MSCI China Small Cap Index will also have an impact on the stock price in the short term. We can keep an eye on the company's trends and seize potential investment opportunities.

Statement of Interest: The content and opinions of this article only represent the author's personal opinion. The author does not hold the stock of the company. The information and analysis provided by the author is for investors' reference only. According to this, the market is at your own risk!

ã€About the Author】

Big director | Glonway · columnist

Engaged in securities investment for five years, and rich experience in domestic and foreign stock research.

The market is always full of illusions, recognize the illusion, and invest in it.

Then exit before the illusion is recognized by the public.

[Essential recommendation]

Huge masterpiece! 50 real estate views shared!

Longguang Real Estate (03380.HK): The dragon is raining, and it is not in the pool.

2016 Real Estate Industry Review: Behind Crazy and Crazy

Hong Kong stocks information · new possibilities

Glonway app is on the line

Sport Ankle Sock,Ankle Sport Socks,Cotton Sport Ankle Socks,Ankle Men Sport Socks

Jingjiang Pingdong Import&Export Co.,Ltd , https://www.jingjiangsocks.com